SIP vs FD Calculator: Which Investment Gives Better Returns? (2026)

SIP vs FD Calculator: Which One Will Make You Wealthier?

In the battle of SIP vs FD calculator, understanding the power of compounding vs. the security of fixed returns is crucial. Discover which investment matches your financial goals.

Investment Details

*Matches your annual SIP total for fair comparison

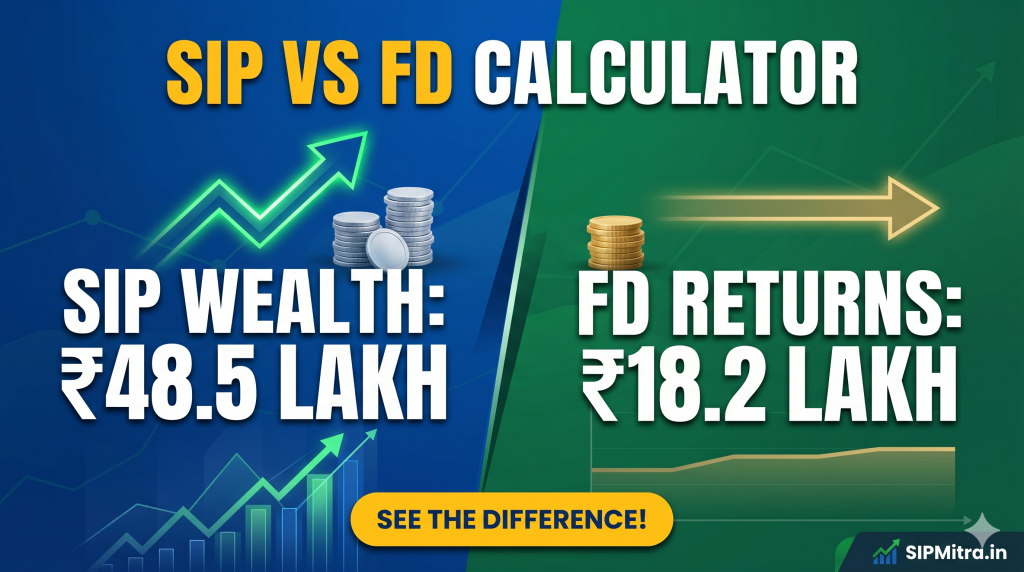

Maturity Comparison

SIP Maturity

₹ 11,50,193

FD Maturity

₹ 8,36,442

The Wealth Difference:

₹ 3,13,751

SIP generates more wealth than FD over the long term.

Introduction: Decoding the SIP vs FD Calculator Debate

When it comes to securing your financial future, the dilemma often boils down to two popular choices: Systematic Investment Plan (SIP) and Fixed Deposits (FD). Investors frequently search for a sip vs fd calculator to understand which instrument will yield higher returns over their chosen time horizon. While FDs have been the traditional favorite for Indian households due to their guaranteed returns and safety, SIPs in mutual funds have gained massive traction for their potential to beat inflation and create massive wealth.

In this comprehensive guide, we won’t just give you a tool. We will dive deep into the mechanics of both investments, analyze risks, discuss taxation, and show you real-life scenarios that prove why choosing the right path today can lead to a difference of lakhs (or even crores) in your retirement corpus.

What is SIP? The Engine of Modern Wealth Creation

A Systematic Investment Plan, or SIP, is a method of investing in mutual funds where you contribute a fixed amount of money at regular intervals—typically monthly. Instead of trying to “time the market” by investing a large sum at once, SIP allows you to benefit from Rupee Cost Averaging.

Key Benefits of SIP:

- Disciplined Saving: SIP automates your investments, ensuring you save before you spend.

- Compounding Power: The earlier you start, the more time your money has to grow exponentially.

- Flexibility: You can start with as little as ₹500 per month.

- No Market Timing: You buy more units when prices are low and fewer units when prices are high.

What is a Fixed Deposit? The Traditional Safety Net

A Fixed Deposit (FD) is a financial instrument provided by banks and Non-Banking Financial Companies (NBFCs) that offers a higher rate of interest than a regular savings account until a given maturity date. It is often considered the safest investment because the returns are guaranteed by the bank and insured up to ₹5 Lakhs by the DICGC.

Why Investors Still Choose FD:

- Guaranteed Returns: You know exactly how much you will get at the end of the tenor.

- Capital Protection: Your principal amount is generally safe from market volatility.

- Liquidity: Most FDs allow for premature withdrawal (though with a small penalty).

- Senior Citizen Benefits: Often offers 0.50% higher interest rates to elderly investors.

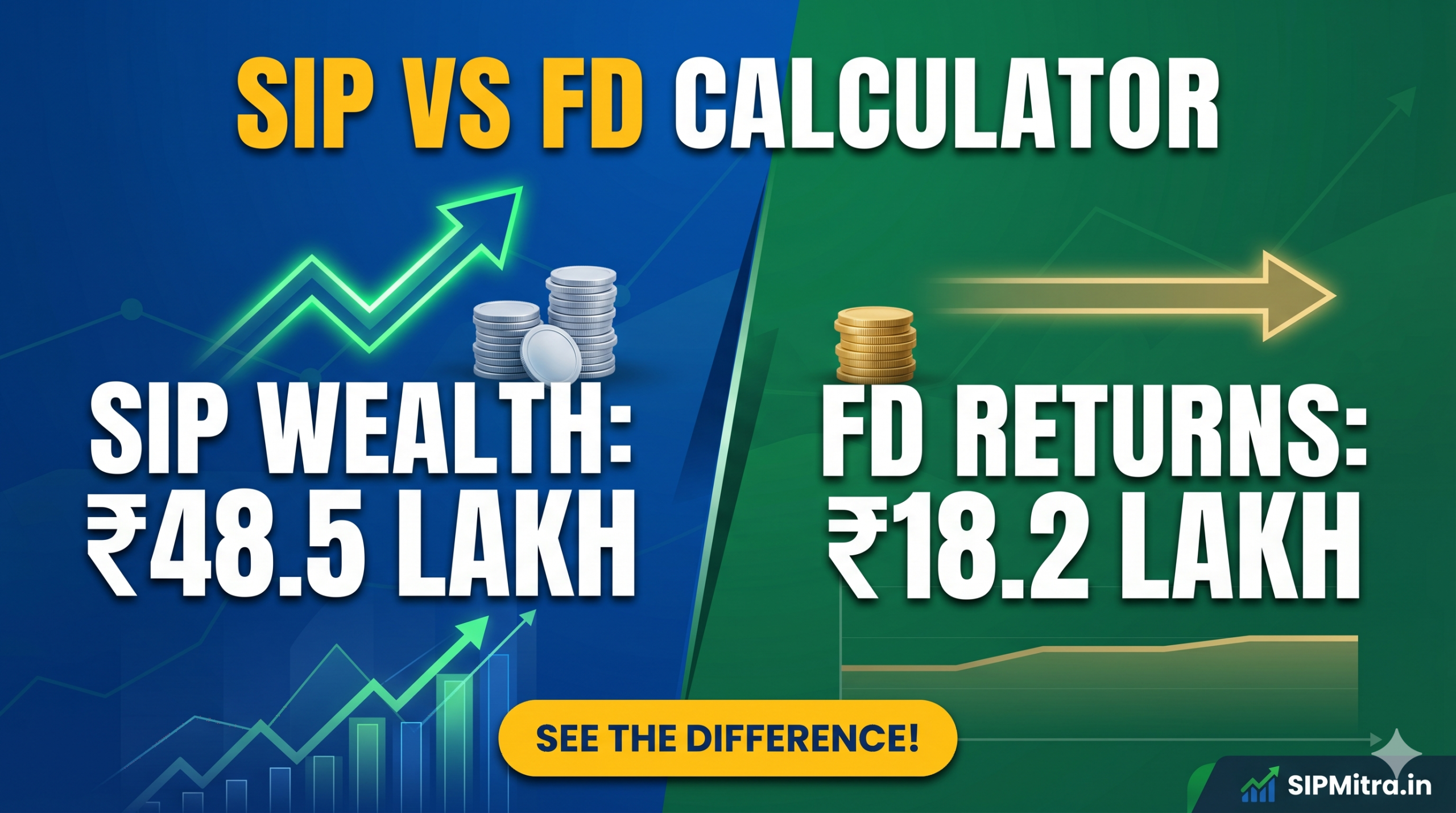

SIP vs FD Returns Comparison: The Real Numbers

To truly understand the impact, let’s use the logic of our sip vs fd calculator. Over a 10-year period, a monthly SIP of ₹10,000 in an equity mutual fund (assuming a conservative 12% CAGR) would grow to approximately ₹23.23 Lakhs. In contrast, the same total investment of ₹12 Lakhs spread over 10 years in an FD (assuming 6.5% interest) would result in a significantly smaller corpus.

| Feature | SIP (Mutual Funds) | Fixed Deposit (FD) |

|---|---|---|

| Expected Returns | 10% – 15% (Historical average) | 5% – 7.5% (Bank dependent) |

| Risk Level | Moderate to High (Market linked) | Very Low (Guaranteed) |

| Inflation Protection | High – Usually beats inflation | Low – Often barely matches inflation |

| Taxation | 12.5% on gains > ₹1.25L (LTCG) | As per your Income Tax Slab |

Risk vs Safety Analysis: Making an Informed Choice

Is the risk of an SIP worth it? Many new investors fear market crashes. However, data shows that over long periods (7+ years), the probability of negative returns in equity mutual funds drops significantly. The sip vs fd calculator highlights the “opportunity cost” of playing it too safe. By choosing the 100% safety of an FD, you are essentially losing out on the purchasing power of your money because of inflation.

For example, if inflation is at 6% and your FD is giving 6.5%, your “real” return is only 0.5%. Meanwhile, an SIP giving 12% provides a real return of 6%, effectively doubling your wealth’s purchasing power much faster.

Taxation Comparison: What Stays in Your Pocket?

Returns are only half the story; taxes are the other half.

FD Taxation

The interest earned on FD is added to your annual income and taxed according to your income tax slab (10%, 20%, or 30%). This can drastically reduce your net returns if you are in the higher tax bracket.

SIP Taxation (Equity Mutual Funds)

- Short Term Capital Gains (STCG): 20% if sold within 1 year.

- Long Term Capital Gains (LTCG): 12.5% if sold after 1 year (exempt up to ₹1.25 Lakhs per year).

Clearly, for long-term investors, SIPs offer a much more tax-efficient way to build wealth.

Which is Better for Long-Term Wealth?

The answer depends on your Financial Goal.

- For Retirement (15-20 years away): SIP is the clear winner. You need the aggressive growth of equity to build a corpus that lasts 20-30 years of non-working life.

- For an Emergency Fund (Immediate): FD or Liquid Funds are better. You need the money to be safe and accessible within 24 hours.

- For Children’s Education (10 years away): A mix of 80% SIP and 20% FD/Debt is usually recommended.

Real Investment Examples

Let’s look at Rohan and Amit. Both are 30 years old and can save ₹10,000 per month.

Amit (The Conservative): Puts ₹10,000 every month in a Recurring Deposit (similar to FD) at 6%. After 20 years, his total investment is ₹24 Lakhs, and his maturity value is ~₹46 Lakhs.

Rohan (The Wealth Builder): Puts ₹10,000 every month in an Equity SIP at 12%. After 20 years, his total investment is also ₹24 Lakhs, but his maturity value is ~₹99 Lakhs!

By simply choosing a different instrument, Rohan ended up with ₹53 Lakhs more than Amit. This is the power our sip vs fd calculator demonstrates.

Frequently Asked Questions (FAQs)

Can I lose money in SIP?

Yes, in the short term, market volatility can cause your portfolio value to go down. However, historically, equity markets have always moved upwards over 7-10 year periods.

Is SIP better than FD for senior citizens?

Senior citizens should prioritize capital protection. While FDs are great for regular income, keeping a small portion (10-20%) in SIPs can help combat inflation during their later retirement years.

How do I use the sip vs fd calculator on this page?

Simply enter your monthly savings amount, expected returns, and the number of years you plan to invest. The calculator will automatically show you the wealth difference between the two options.

Conclusion: Take Action Today

The data is clear. While FDs provide comfort, SIPs provide wealth. To reach your financial dreams—whether it’s a dream home, international travel, or an early retirement—you need your money to work as hard as you do.

Don’t let your savings rot in a low-interest account. Use the sip vs fd calculator insights to rebalance your portfolio.

अगर आप long-term wealth creation चाहते हैं, तो Early Retirement with SIP strategy भी आपके लिए काफी फायदेमंद हो सकती है।